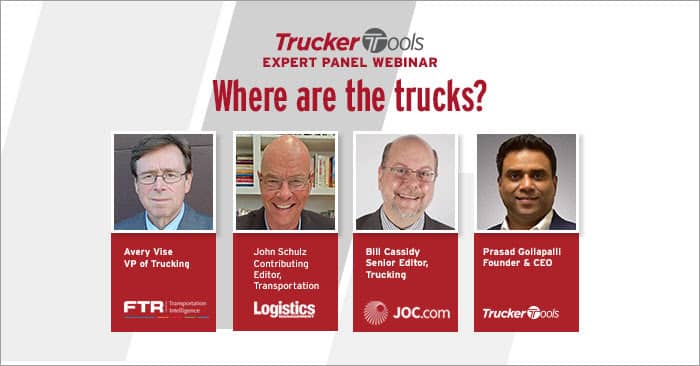

In a recent webinar entitled “Where Are the Trucks?,” Trucker Tools’ CEO and founder Prasad Gollapalli moderated a panel discussion on what freight brokers and 3PLs can expect from the truck capacity market in the remaining months of 2021. The panel included FTR Transportation Intelligence’s VP of Trucking Avery Vise, JOC’s Senior Editor for Trucking and Domestic Transportation Bill Cassidy, and Logistics Management Magazine’s Trucking Industry Expert and Contributing Editor John Schulz. The panel’s discussion centered on Q1 capacity challenges, the insights gained from Q1 and predictions regarding the U.S. truck capacity market for the remainder of the year.

Q1 2021 Challenges

Our panelists agreed that the first quarter of the year was a challenging one for shippers, brokers/3PLs and carriers. Usually Q1 is a post-holiday lull typified by lower demand and rates. Not so in 2021. This year’s first quarter saw port congestion on the West Coast disrupt freight markets and freight rates increased significantly. Obviously, the COVID-19 pandemic and changing consumer buying patterns also have put pressure on freight markets, as has the driver shortage.

“What you hear when you talk to long-time trucking execs is that they’ve never seen a situation like this before,” said Schulz. “There’s a capacity shortage, there’s a driver shortage and there’s a computer chip shortage affecting truck manufacturers. Capacity is king. Trucking is a very cyclical industry and capacity was at a premium in the first quarter, which is usually the slowest time for volumes. COVID is probably the primary reason, but it’s not the only reason.”

“What you hear when you talk to long-time trucking execs is that they’ve never seen a situation like this before,” said Schulz. “There’s a capacity shortage, there’s a driver shortage and there’s a computer chip shortage affecting truck manufacturers. Capacity is king. Trucking is a very cyclical industry and capacity was at a premium in the first quarter, which is usually the slowest time for volumes. COVID is probably the primary reason, but it’s not the only reason.”

One of the poll questions asked during the webinar was, “Are you still experiencing a capacity crunch in your brokerage?” It’s worth noting that 64 percent of attendees reported that finding capacity is still very difficult, while 36 percent said finding capacity is not as bad as it had been in previous months.

“We’re in an extremely unusual time,” said Cassidy. “There are long delays and congestion at ports, with shippers paying double what they paid a year ago. It’s something that we haven’t seen at this time of year in quite a while. You add that into what’s happening on the ground with tightening trucking capacity at a time of year when the market is usually more stable. The big challenge is just finding capacity for shippers. A lot of companies are happy if they can find capacity right now on land or sea, and are worried about how they’re going to pay for it after they get it.”

What We’ve Learned from Q1

According to the panel, one of the things that Q1 has taught us is that the FMCSA’s new Drug & Alcohol Clearinghouse is having an effect on the number of drivers available to move freight, which impacts available truck capacity. Looking at industry employment data also gives us insight into a broader trend within trucking and logistics.

“Overall, the first year of the drug and alcohol clearinghouse cost about 48,000 drivers who were in the market in January 2020 who are no longer in the market,” Vise said. “There was a surge at the end of 2020 in the number of drivers who were disqualified. However, I think when we get the data on March, we’re going to see an increase in payroll employment in trucking and I think it will be substantial. All of this matters because one thing we are seeing is a shift in capacity from the motor carriers/trucking companies into the 3PL and intermediary environment. It represents a shift in capacity into the intermediary environment and away from the traditional trucking environment. I think that’s got a lot of implications.”

“Overall, the first year of the drug and alcohol clearinghouse cost about 48,000 drivers who were in the market in January 2020 who are no longer in the market,” Vise said. “There was a surge at the end of 2020 in the number of drivers who were disqualified. However, I think when we get the data on March, we’re going to see an increase in payroll employment in trucking and I think it will be substantial. All of this matters because one thing we are seeing is a shift in capacity from the motor carriers/trucking companies into the 3PL and intermediary environment. It represents a shift in capacity into the intermediary environment and away from the traditional trucking environment. I think that’s got a lot of implications.”

Cassidy noted that early in the year, shippers were looking to postpone contract negotiations. When rates spiked again in January, a lot of shippers changed their minds and signed contracts in the fourth quarter of 2020 and first quarter of 2021. Cassidy contends that these contracts signed early on the year will likely bring a degree of normalcy to the spot market in 2021.

The Rest of 2021

“For at least the short term, carriers are kings because they control the capacity to a great extent,” said Shulz. “In terms of rates, I think strong rates will definitely continue through this calendar year. Carriers are getting load double-digit increases in contract renewals on both the LTL side and the truckload side. They’re being very cautious and picky over who they’re doing business with. At least through the end of this calendar year, I consider it a very strong and positive rate environment for carriers. It’s their turn. As the pendulum swings, they have it on their side now.”

In the webinar, Vise contended that capacity is likely to loosen during the remaining months of 2021. He said that he sees the training of new CDL drivers as critical to stabilizing capacity markets. Vise advised that continued aggressive pay packages for drivers will help loosen capacity. In contrast, Cassidy said that he anticipates tight capacity to last through the end of 2021 and as long as the COVID-19 pandemic continues disrupting markets. He said that perhaps by summer, we will return to something that looks more like normal, but that the pandemic will continue to have ripple effects on freight and capacity.

“We will continue to see issues regarding production, the availability of overseas shipping and shipping capacity, and weird inventory patterns,” said Cassidy. “The problem with drivers will continue to be an issue, even if hiring does increase in March. This is the first time we’ve had a year-over-year driver shortage since 2008 and 2009. If we have strong hiring and get capacity levels back to where they were a year ago, that will be a great stride. There’s also a high demand for e-commerce and local general freight trucking, so there will be a lot of competition for drivers.”

“We will continue to see issues regarding production, the availability of overseas shipping and shipping capacity, and weird inventory patterns,” said Cassidy. “The problem with drivers will continue to be an issue, even if hiring does increase in March. This is the first time we’ve had a year-over-year driver shortage since 2008 and 2009. If we have strong hiring and get capacity levels back to where they were a year ago, that will be a great stride. There’s also a high demand for e-commerce and local general freight trucking, so there will be a lot of competition for drivers.”

For more insights and the rest of our panel’s capacity discussion, watch “Where Are the Trucks?” Schedule a free demo of Trucker Tools’ real-time visibility platform, digital freight matching and innovative load booking tool Book-It-Now®.